Intro

Discover what reserves are, including types like cash reserves, and learn how reserve requirements impact financial institutions, asset management, and economic stability.

In the realm of finance, accounting, and business, reserves play a crucial role in ensuring the stability and security of companies, institutions, and even entire economies. Reserves refer to the amount of money or assets that are set aside for future use, typically to meet unexpected expenses, liabilities, or financial obligations. The importance of reserves cannot be overstated, as they provide a safeguard against potential risks, uncertainties, and downturns in the market.

Reserves can take many forms, including cash, investments, and other liquid assets. They are often held by companies, banks, and other financial institutions to maintain liquidity, absorb potential losses, and ensure compliance with regulatory requirements. In the context of banking, for example, reserves are used to meet the demands of depositors, maintain capital adequacy, and absorb potential losses from loan defaults. Similarly, companies may maintain reserves to cover unexpected expenses, such as lawsuits, natural disasters, or economic downturns.

The concept of reserves is not limited to the financial sector; it is also relevant to individuals and households. For instance, having a personal emergency fund or savings account can provide a sense of security and stability, allowing individuals to cover unexpected expenses, such as medical bills, car repairs, or losing a job. In essence, reserves serve as a buffer against uncertainty, providing peace of mind and financial flexibility.

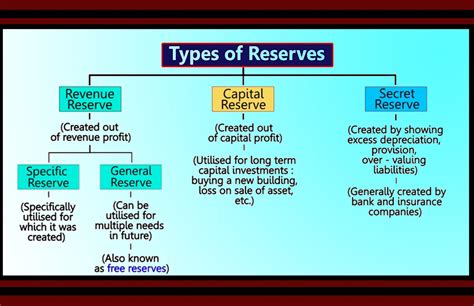

Types of Reserves

There are several types of reserves, each serving a specific purpose. Some of the most common types of reserves include:

- Cash reserves: These are the most liquid type of reserve, consisting of cash and cash equivalents, such as commercial paper, treasury bills, and other short-term investments.

- Investment reserves: These reserves are invested in assets, such as stocks, bonds, and real estate, to generate returns and grow the reserve over time.

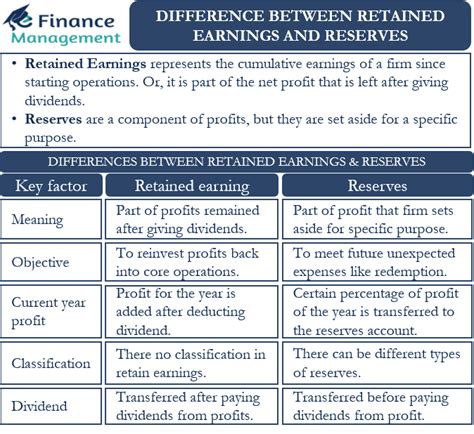

- Retained earnings reserves: These reserves represent the accumulated profits of a company that are retained and reinvested in the business, rather than being distributed to shareholders.

- Contingency reserves: These reserves are set aside to cover unexpected expenses or losses, such as natural disasters, lawsuits, or economic downturns.

- Regulatory reserves: These reserves are required by regulatory bodies, such as the Federal Reserve, to ensure that banks and other financial institutions maintain adequate capital and liquidity.

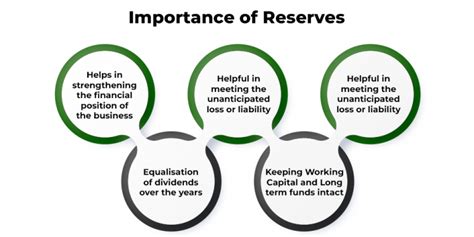

Importance of Reserves

The importance of reserves cannot be overstated. Reserves provide a number of benefits, including:

- Financial stability: Reserves help to maintain financial stability by providing a buffer against unexpected expenses, losses, and downturns in the market.

- Liquidity: Reserves ensure that companies and institutions have sufficient liquidity to meet their financial obligations, such as paying debts, meeting payroll, and maintaining operations.

- Risk management: Reserves help to manage risk by providing a cushion against potential losses, such as loan defaults, natural disasters, and economic downturns.

- Regulatory compliance: Reserves are often required by regulatory bodies to ensure that companies and institutions comply with capital and liquidity requirements.

- Investment opportunities: Reserves can provide a source of funds for investment opportunities, such as expansion, research and development, and acquisitions.

How Reserves Work

Reserves work by providing a pool of funds that can be drawn upon to meet unexpected expenses, losses, or financial obligations. The process of establishing and maintaining reserves typically involves the following steps:

- Identification of risks: Companies and institutions identify potential risks and uncertainties that may impact their financial stability.

- Assessment of risks: The potential impact of each risk is assessed, and a determination is made as to the amount of reserves required to mitigate the risk.

- Establishment of reserves: Reserves are established and funded through a variety of means, such as retained earnings, investments, and cash flows.

- Maintenance of reserves: Reserves are regularly reviewed and updated to ensure that they remain adequate to meet potential risks and uncertainties.

- Use of reserves: Reserves are drawn upon as needed to meet unexpected expenses, losses, or financial obligations.

Benefits of Reserves

The benefits of reserves are numerous and can have a significant impact on the financial stability and security of companies, institutions, and individuals. Some of the most significant benefits of reserves include:

- Reduced risk: Reserves help to reduce the risk of financial instability and insolvency by providing a buffer against unexpected expenses and losses.

- Increased liquidity: Reserves ensure that companies and institutions have sufficient liquidity to meet their financial obligations and maintain operations.

- Improved financial flexibility: Reserves provide a source of funds that can be used to take advantage of investment opportunities, such as expansion, research and development, and acquisitions.

- Enhanced credibility: Companies and institutions that maintain adequate reserves are viewed as more credible and financially stable, which can enhance their reputation and attract investors and customers.

- Regulatory compliance: Reserves help companies and institutions to comply with regulatory requirements, such as capital and liquidity standards.

Challenges and Limitations of Reserves

While reserves are an essential component of financial stability and security, there are also challenges and limitations associated with maintaining them. Some of the most significant challenges and limitations include:

- Opportunity costs: Maintaining reserves can result in opportunity costs, as the funds are not being used to generate returns or invest in growth opportunities.

- Inflation: Reserves can be eroded by inflation, which can reduce their purchasing power and value over time.

- Liquidity risks: Reserves can be subject to liquidity risks, such as the inability to access funds when needed or the risk of losses due to market fluctuations.

- Regulatory requirements: Regulatory requirements can be complex and burdensome, making it challenging for companies and institutions to maintain adequate reserves.

- Funding constraints: Maintaining reserves can be challenging for companies and institutions that face funding constraints, such as limited access to capital or cash flow constraints.

Best Practices for Maintaining Reserves

To maintain effective reserves, companies and institutions should follow best practices, such as:

- Regularly reviewing and updating reserves: Reserves should be regularly reviewed and updated to ensure that they remain adequate to meet potential risks and uncertainties.

- Diversifying reserves: Reserves should be diversified to minimize the risk of losses due to market fluctuations or other factors.

- Maintaining liquidity: Reserves should be maintained in a liquid form to ensure that they can be accessed when needed.

- Complying with regulatory requirements: Companies and institutions should comply with regulatory requirements, such as capital and liquidity standards.

- Monitoring and reporting: Reserves should be regularly monitored and reported to ensure that they are adequate and effective.

Reserves Image Gallery

What are reserves?

+Reserves refer to the amount of money or assets that are set aside for future use, typically to meet unexpected expenses, liabilities, or financial obligations.

Why are reserves important?

+Reserves are important because they provide a buffer against unexpected expenses, losses, and downturns in the market, helping to maintain financial stability and security.

What are the different types of reserves?

+There are several types of reserves, including cash reserves, investment reserves, retained earnings reserves, contingency reserves, and regulatory reserves.

How do reserves work?

+Reserves work by providing a pool of funds that can be drawn upon to meet unexpected expenses, losses, or financial obligations, helping to maintain financial stability and security.

What are the benefits of reserves?

+The benefits of reserves include reduced risk, increased liquidity, improved financial flexibility, enhanced credibility, and regulatory compliance.

In conclusion, reserves are a crucial component of financial stability and security, providing a buffer against unexpected expenses, losses, and downturns in the market. By understanding the different types of reserves, their importance, and how they work, companies and institutions can maintain effective reserves and ensure their financial stability and security. We invite you to share your thoughts and experiences with reserves in the comments section below. Additionally, if you found this article informative and helpful, please share it with others who may benefit from this knowledge.